“Nil satis nisi optimum” Everton Football Club motto

How Everton’s owners must lament that history has bequeathed them as a motto a Latin phrase meaning “Nothing but the best will do” because, since their 1995 FA Cup win, Everton really haven’t been the best at anything. But it is a stick with which to beat an underperforming club, and so it was with the acronym NSNO that disaffected Everton fans appended their banner of dissent as it flew by St Mary’s Stadium last week.

The 3-0 away victory against Southampton, a team that finished seventh last season, rather took the wind from beneath the wings of the plane of protest (hired at a cost of £2,000 – €2750, $3150 – by all accounts). Still, a thoroughly modern statement was made: ‘Kenwright & Co #Timetogo NSNO’. Two days later the chairman Bill Kenwright would be marking 24 years as a director of Merseyside’s second-most-successful club and there are no signs of him being dislodged. The aerial demonstration will prove entirely futile, of course.

The reasons are many. First of all we must ask the question: are Everton really underperforming under Kenwright? And the fact is, no they are not. If anything they are exceeding expectations. Take a look at the table below.

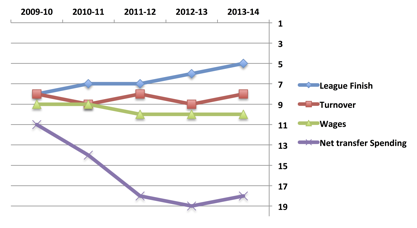

Everton’s key metrics relative to the Premier League

The most important statistic is their league position, which has been highly creditable. Between 2009-10 and 2013-14 (the most recent season for which financial data are available), Everton finished in the top eight every year, with improving returns each year. This despite having to manage the succession of David Moyes’s departure for Manchester United after 11 years in the Goodison Park dugout.

Last season, the trend dipped as the club finished 11th. But that was roughly on a par with reasonable expectations, given how the club’s wage bill had been only the 10th biggest in the Premier League. Indeed, net transfer spending had been among the bottom three for the previous three years and never in the top 10 in the previous five.

Now disgruntled Everton fans might consider this to be an area ripe for criticism. But as the old football axiom goes, the league table does not lie, and as the chart above shows, that past lack of investment did not have a particularly negative impact on football performance.

So what were the reasons for the reduced transfer activity? They can be traced back to a piece of paper signed in March 2002, when the club consolidated all its debts with Prudential with a £30 million (€41.2m, $47.2m) term loan. At the time they had more mortgages than a distressed Monopoly player: the Puma sponsorship money had been advanced, the transfer fee from L